Rare Earth Metals Were Supposed To Be The 'Can't-Lose' Investment Of The Decade — Look How That Turned Out

- SEP. 16, 2014, 11:52 AM

Shares of rare earth mining company Molycorp are down more than 70% in 2014.

But the decline of Molycorp began quickly and brutally in 2011.

Molycorp went public in July 2010 at $14 per share, right as the price of rare earth minerals started to take off.

The price of Molycorp shares quintupled within a year, and peaked at $74 in 2011.

But over the last three years, the stock has been on a steady march towards $0.

The 2010 surge in rare earth prices prompted ZeroHedge to write: "Ever heard of the oxides of Lanthanum, Cerium, Neodymium, Praseodymium and/or Samarium? With price surges between 250% and 600% in one quarter, you may wish you have."

Rare earth elements are used to make lasers, magnets, and plasma TVs, among other products. These elements also aren't exactly rare, but aren't found in huge concentrations the way coal is found en masse in one spot, making them expensive to mine.

Most rare earth productions was coming from China, which created a problem with making a fair market in rare earth mineral prices. But despite this concentration, a Bloomberg report from June 2011 cited industry analysts who saw the high prices continuing as supply failed to meet demand.

Per Bloomberg:

"Dudley Kingsnorth, a former rare earths project manager and now chief executive officer of Perth-based advisory Industrial Minerals Co. of Australia. 'There might be an element of speculation but I think the price rises have been driven by people who are desperate for the product.' ... Companies such as Molycorp Inc. and Lynas Corp. are rushing to restart mothballed projects to meet the gap in supply. Greenwood Village, Colorado-based Molycorp plans to bring its Californian mine into production in the second half of 2012 and double the mine’s annual capacity to 40,000 metric tons by the end of 2013… 'Until such time as Lynas and Molycorp are on-stream in the next two or three years, I don’t see much relief' from high prices, Kingsnorth said. 'Chinese export quotas are less than world demand.'"

ZeroHedge wrote that this increase was due to China cornering the rare earth market. Either way, it didn't work out.

By September 2011, Molycorp shares were in a bona-fide free-fall. And while some analysts were cutting expectations for the stock (JPMorgan cut its price target to $66 from $105, but still), other firms were still rushing to the company's defense.

On Tuesday, shares of Molycorp were trading at around $1.50.

In an investor presentation in June, Molycorp included the following chart showing the decline in the price of rare earth material.

When you compare the price of Molycorp stock and the price of rare earth material, the two charts look similar. This is not a coincidence.

Molycorp

Molycorp Yahoo Finance

Yahoo Finance

On Sept. 11, Oaktree Capital Management threw the company a $400 million lifeline through a combination of credit lines and the sale and leaseback of company equipment. The agreement included $250 million of financing currently funded, with the remaining $150 million available in April 2016 if the company meets certain production and profitability goals.

Under the Oaktree agreement, Molycorp must achieve two straight quarters of consolidated adjusted EBITDA of at least $20 million. In the second quarter of 2014, Molycorp's consolidated adjusted OIBDA was a loss of $2 million.

OIBDA, or operating income before depreciation, and amortization, is a similar but not exactly the same measure as EBITDA, or earnings before interest, taxes, depreciation, and amortization. Companies usually report one or the other, and the difference is where the calculation starts.

OIBDA uses a company's operating income rather than earnings, which could include non-operating income or items that don't recur regularly. In the second quarter, Molycorp wrote off about $20 million of what it considers non-recurring items, so using operating income was a more friendly starting point for calculating profit.

Eventually, though, Molycorp will have to figure this out.

But again, the core problem Molycorp has been facing goes beyond its financing agreements or commitments. The price of rare earth materials crashed and hasn't meaningfully recovered.

In that June presentation Molycorp, citing data from IMCOA/Curtin University, said that rare earth demand is expected to grow at 6%-10% annually through 2017. And if this doesn't come through, the future likely remains bleak for Molycorp.

(h/t @BarbarianCap — a great follow for thoughts on the markets — for alerting us to Molycorp's demise)

Read more: http://www.businessinsider.com/molycorp-decline-in-2014-2014-9#ixzz3DgpG6Div

OAKTREE CAP GROUP LLC UNITS CL A (OAK)

49,97 USD

+2,90% | +1,41

12/08/2014 22:04

MOLYCORP INC DELAWARE COM USD0.001 (MCP)

2,19 USD

-5,60% | -0,13

12/08/2014 22:01

Bloomberg News

Oaktree Gives Molycorp’s Mine More Time: Distressed Debt

Oaktree Capital Management LP (OAK:US) is throwing Molycorp Inc. (MCP:US) a lifeline with $400 million of loans that gives the company cash to operate until the first quarter of 2016 as its Mojave Desert mine moves toward full production.

The financing didn’t come cheap: Molycorp will pay an interest rate of 12 percent, the highest on a loan made in the U.S. this year, according to data compiled by Bloomberg. Not only that, Oaktree gets warrants to buy 10 percent of the miner of rare-earth minerals, which are used in electronic devices from Apple Inc.’s iPads to Raytheon Co.’s Tomahawk missiles.

Molycorp may see that as a small price to pay. It has been unprofitable for the past 10 quarters and would have run out of cash around the start of next year, before it could bring its Mountain Pass mine to full production, Bloomberg data show. The company’s crown jewel, plagued by development setbacks that have soaked up $1.5 billion of investments, has the potential at full output to generate enough cash to end the crunch, according to Kevin Starke, an analyst at CRT Capital Group Inc. in Stamford, Connecticut.

“It’s like you move the ball closer to the goal line, but the kicker has a sprained ankle,” Starke, who specializes in distressed investments, said by telephone.

Burn Rate

At the current rate of cash burn, factoring in the interest expense from the new debt, Greenwood Village, Colorado-based Molycorp is likely to run out of cash in the first quarter of 2016 if Mountain Pass doesn’t go fully online and rare-earths prices don’t improve, said Starke.

While the new financing matures in five years, that would be accelerated if the company doesn’t repay $230 million of 3.25 percent convertible bonds maturing in June 2016, Chief Financial Officer Michael Doolan said on an Aug. 7 conference call to discuss second-quarter earnings with analysts and investors. The loan has a payment-in-kind feature that allows 5 percentage points to be paid in additional debt, he said.

Oaktree will disburse $110 million as a loan and $140 million as part of a sale-and-leaseback transaction for some of Molycorp’s equipment when the financing closes, Doolan said. That’s expected “in the next several weeks,” President and Chief Executive Officer Geoffrey Bedford said on the call.

The remaining $150 million will depend on whether the company achieves two specific targets, which Doolan didn’t disclose. He said the company was “comfortable” with its ability to achieve them.

Alyssa Linn, a spokeswoman for Oaktree at Sard Verbinnen, didn’t reply to an e-mail seeking comment. Jim Sims, a spokesman at Molycorp, declined to comment.

Cash Level

The new capital would boost the company’s cash position to $406 million, adding to the $156 million in cash (MCP:US) it reported for June 30, Bloomberg data show.

Free-cash flow (MCP:US), or the amount the company makes from operating activities less capital expenditures, was negative $533.7 million last year. The miner would have $1.72 billion in total debt after the $250 million of loans are in place and would have about $104 million in interest expense, Starke said.

“Putting a new first-lien loan in says Oaktree has some confidence in the industry turnaround,” Starke said. On the other hand, were Molycorp to restructure, a lender would try to position itself to control the company. “Oaktree’s move into the senior debt is a perfect expression of that strategy,” Starke said.

First-lien debt has the senior claim on assets pledged to secure it. Oaktree thus vaults to the top position among Molycorp’s creditors by making the loans.

Oaktree, founded by Howard Marks, also owned as much as $5 million of Molycorp’s 3.25 percent convertibles at the end of March, Bloomberg data show. The bonds, which would convert to common stock once Molycorp’s shares surpass $71.40, traded at 73.5 cents on the dollar to yield 21.4 percent on Aug. 5, according to Trace, the bond-price reporting system of the Financial Industry Regulatory Authority.

The shares fell 1.69 percent yesterday to $2.32, leaving them down 59 percent(MCP:US) for the year. The Bloomberg Rare Earth Mineral Index, 11 percent of which is accounted for by Molycorp, is down 34 percent this year.

Molycorp’s $650 million of 10 percent first-lien notes maturing June 2020 fell 0.8 cent to 86.5 cents on the dollar for a 13.4 percent yield yesterday. That’s more than 11 percentage points higher than comparably dated Treasuries, above the 10 percent threshold considered distressed. Those notes traded at 88 cents for a yield of 12.99 percent on Aug. 4.

‘Interesting Bet’

The deal with Oaktree didn’t “immediately” affect Molycorp’s credit standing at Moody’s Investors Service, which said in an Aug. 8 statement that there were “uncertainties over the eventual execution and the precise terms of the arrangement.

Moody’s rates Molycorp Caa2, the middle of its category of debt with ‘‘very high credit risk,’’ and Standard & Poor’s grades it an equivalent CCC, Bloomberg data(MCP:US) show.

The miner has been plagued by cost overruns and delays in its Mountain Pass facility, which boasts the largest rare-earth metals deposit outside of China, helping erode the $3.8 billion the company raised in 10 bond and equity offerings since 2010, Bloomberg data show.

The 17 rare-earth elements are used in electronic devices. Prices have plunged in the past three years with representative rare earths such as lanthanum oxide falling 89 percent from its June 2011 high and neodymium oxide and dysprosium oxide each down 80 percent.

Bedford said on the call that management intends to ‘‘complete this production ramp as quickly as possible’’ and is confident current demand will match the company’s target output of 23,000 metric tons a year. The mine has been producing at an annual rate of 12,000 tons to 13,000 tons, JPMorgan analysts led by Michael Gambardella, said in a May 9 report.

Molycorp reported last week second-quarter revenue of $116.9 million, compared with analyst estimates of $131 million, Bloomberg data show. It posted a $86.1 million loss before interest, taxes, depreciation and amortization.

‘‘For Oaktree, it’s an interesting bet on a turn in the industry and the runway is pretty short and narrow,” Starke said.

To contact the reporter on this story: Jodi Xu in New York at jxu205@bloomberg.net

To contact the editors responsible for this story: Shannon D. Harrington at sharrington6@bloomberg.net Mitchell Martin, Richard Bravo

Molycorp: Smart Money Bets On Restructuring, Shares Plummet 17%

Summary

- Apollo Global is betting that Molycorp will have to restructure its long-term debt.

- Molycorp's bankruptcy risk weighed on investors who drove the stock down 17% yesterday.

- The stock may have more room to fall if Molycorp seeks to raise equity capital or has a disappointing Q2 earnings report.

Image Source: "Trading Places" The Movie

Bloomberg News reported Tuesday night after hours that legendary hedge fund investor Leon Black of Apollo Global Management LLC (NYSE:APO) has been snapping up Molycorp Inc's (NYSE:MCP) convertible bonds in order to gain control of the rare earth miner if it defaults on its debt. According to Bloomberg, Apollo controls over 20% of Molycorp's $230 million 3.25% convertible bonds due in 2016. Black is the quintessential definition of "smart money." I am personally a Michael Milken junkie and have read everything available on him and his former firm, Drexel Burnham Lambert. That said, I have known about Black since he was a Managing Director at Drexel in the late 1980s. If he is betting that Molycorp could be headed for bankruptcy that can't be good, right?

The market seemed to agree with Black's assessment with a huge sell-off yesterday. Molycorp fell $0.38 to $1.88 per share, a 17% decline from its previous close of $2.26 per share. Trading volume spiked to 21.1 million shares; average trading volume is 5.5 million. In early June the 3.25% convertibles traded at about 69 cents on the dollar. Based on Molycorp's cash burn - the company experienced Q1 cash out flows of $78 million - I did not think the pricing of the bonds reflected the company's bankruptcy risk. There were also reports that the bonds were traded up after Lynas Corporation's (OTCPK:OTCPK:LYSCF) (OTCQX:OTCQX:LYSDY) May press release stating it had raised equity capital; apparently, bond investors assumed Molycorp could raise equity in a similar fashion as its rare earth competitor. On my previous article I called the bonds mullet money or "dumb money":

Investors should buy bonds based on what they are actually worth. By buying Molycorp bonds with the assumption the company will raise equity in a similar manner as Lynas is foolhardy. Molycorp's bonds do not reward investors for the risk involved. Therefore, I believe bond holders are providing mullet money.

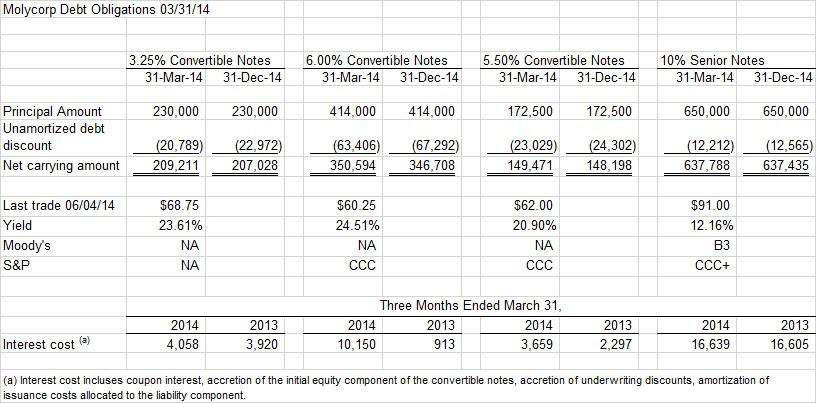

The following chart illustrates Molycorp's long-term debt:

(click to enlarge)

Is Dilutive Event Imminent?

Molycorp's cash out flows and operating losses have gone unabated for several quarters. Molycorp reported a loss of $88.1 million for Q1 2014, compared to a loss of $39.0 million for Q1 2013. Its cash on hand dwindled to about $236 million; that comes after two previous capital raises in 2013. If the company does not find a solution to its cash burn, it runs the risk of defaulting on its bonds and being taken over by Apollo and other bond holders. The question for longs is, "If Molycorp raises capital, how dilutive will it be?" The play is to buy the stock at a price you can live with and hope the rare earth miner survives, or try to buy the stock at a lower price after a potential dilutive event.

Conclusion

Apollo is betting that Molycorp will default on its debt obligations. Now that the smart money has made its play, the market has come to the realization that Molycorp may need to seek a dilutive event or face bankruptcy. I would advise investors to avoid the stock and buy it after the Q2 earnings report in August gives more visibility on the company's cash needs.

Editor's Note: This article covers a stock trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Molycorp: A Top $5 Stock Pick For A 'January Effect' And Short-Covering Rally

Molycorp, Inc. (MCP) shares were surging ever higher in 2011, and that momentum and investor optimism took the stock to over $70 per share for a while. At that time, many investors seemed to believe that rare earth minerals were going to be the next big thing, but clearly that level of optimism was excessive. More recently, many investors have become decidedly bearish by shorting the stock, and many others have sold out of pure frustration. However, as most investors realize, timing is everything when it comes to investing, and that seems particularly true when investing in Molycorp, Inc. For a number of reasons, it could now be the right time to buy this stock, here's why:

1) Molycorp shares have a 52-week low of $4.51, and a 52-week high of $11.81. With the stock now trading just below $5, it is close to the lows. Investors who bought this stock when it was trading for $30, $40, $50, $60 and even over $70 in 2011 have losses, and investors who bought it even this year when it was trading at more than double the current price, also have losses. That makes this stock an ideal candidate for tax-loss selling which happens in the last few weeks of each year as investors sell "losers" in order to offset taxes on their winning trades. By taking a look at the chart below, it clearly shows a stock that has traded (for the most part) in a range between $5 to $8 per share from April to October. However, more recently (in the peak tax-loss selling months of November and December), this stock has been under obvious pressure which has pushed it just below $5, and kept it from making some of the big rallies it has made multiple times, before tax-loss selling season began. However, that could change since tax-loss selling pressure is about to end in just a few days. The end of tax-loss selling pressure could greatly impact Molycorp shares and make it an ideal candidate for a "January Effect Rally".

(click to enlarge)

2) When looking for stocks that could rebound significantly when tax-loss selling pressure ends, it can be even more rewarding to consider ones that have an above-average level of short interest. According to Shortsqueeze.com, there are about 59 million shares short in Molycorp. This is significant because the average trading volume is about 3.6 million shares, which means the short interest is equivalent to around 16 days worth of trading volume. It is also significant because the short position represents nearly 32% of the float. Now there are two more points to consider: 1) If the stock can trade for nearly $5 per share in the midst of weeks of (probably very heavy) tax-loss selling pressure, it stands to reason that it will trade for more once this selling pressure ends on December 31. 2) Many shorts have significant gains in Molycorp this year and it also stands to reason that it could be desirable (but probably not smart) for them to wait until January to cover since this will allow them to defer taxes on the gains for an additional year. For these reasons, Molycorp shares could be poised for big gains into January since the end of tax-loss selling should help the stock rebound, and in turn, this sudden strength could cause some shorts to cover. Finally, buying pressure from shorts who were waiting until January to cover in order to defer taxes could also lead to a short-covering rally in this stock. Again, timing is everything, and these reasons lead me to believe that the time is right to buy now.

Now let's look at some longer-term reasons to consider buying Molycorp: This company is one of the world's largest rare earth producers and it is based in Mountain Pass, California. Since Molycorp and "Project Phoenix" are located in California, this company does not have the type of geopolitical risks that other mining companies are exposed to. This reduces risks for investors and it makes Molycorp well-positioned to supply the U.S. and the world with rare earth minerals which are used in products ranging from televisions, mobile phones, magnets, lighting, catalytic converters for cars, and more. The demand for rare earths is poised to grow over time, especially as the global economy improves and as the population expands.

Molycorp has made significant investments to develop its rare earth mines and the company is expected to see rapid revenue growth.Analysts expect revenues to surge from about $579 million in 2013, to around $865 million in 2014. That is a jump of roughly 50% and strong growth rates could continue for years to come as production increases and prices improve. This growth is what should help to turn the corner in terms of profits as analysts expect the company to lose about $1.09 in 2013, but see losses of only 27 cents for 2014. While losses are a potential downside risk for investors to consider, the rapid revenue growth mitigates a lot of this risk. Furthermore, the company is expected to be cash flow positive as soon as sometime in 2014. Another potential downside risk to consider is the pricing for rare earths. If the global economy were to experience another recession, the demand could drop and impact revenues and profit margin for Molycorp. However, the economy does not appear to be at risk of recession now, and demand for the type of tech and other products that use rare earths seems likely to grow.

In October, analysts at Cowen and Company raised the price target on this stock to $8.60. With the stock now trading for nearly $5 per share, this would imply potential gains of around 80%. Analysts usually set price targets for the next 12 months, so if that target is reached it would be quite a strong gain for investors. However, even that could be too conservative as Jason Bond makes a solid case for Molycorp shares to be a multi-bagger in about 18 months in this article. In the short term, I believe this stock is poised for a major rebound in January as tax-loss selling ends and as shorts cover. These forces could push the stock back up towards $5.96 which is the 200-day moving average.

Molycorp is clearly a compelling investment as a short-term rebound candidate and it has long-term growth potential. Some industry watchers have even suggested that Molycorp could be an attractive takeover targetfor a global manufacturing giant like Nissan (OTCPK:NSANY) or Siemens (SI), as this would secure access to the rare earths used by these companies. At this time, I am focused on stocks like Molycorp which have significant upside potential in a January Effect rally. To read about another metals mining (molybdenum) stock trading for $1, that also has January Effect rally in the short term and multi-bagger potential in the longer term, you can read more on that in this article.

Here are some key points for Molycorp, Inc.

Current share price: $4.85

The 52 week range is $4.51 to $11.81

Current share price: $4.85

The 52 week range is $4.51 to $11.81

Data is sourced from Yahoo Finance. No guarantees or representations are made. Hawkinvest is not a registered investment advisor and does not provide specific investment advice. The information is for informational purposes only. You should always consult a financial advisor.

Aucun commentaire:

Enregistrer un commentaire