PHILLIPS 66 (PSX)

Aug. 23, 2015 11:21 AM ET

Summary

- Phillips 66 has seen its share price fall over the past few days.

- The company has significant growth plans, especially in the midstream sector.

- Phillips 66 has done an impressive job of rewarding shareholders through buybacks and increasing dividends.

Introduction

The oil crash has struck all and struck hard. It has been relentless and unforgiving, and just when people thought a bottom was near, something came up and made it take another hit. In fact, energy is one of the few sectors in the S&P 500 that is not hitting fresh highs every other day - or so I seem to hear (last week was an exception).

But just like the finance stocks in 2008, every crashing sectors have stocks to pick and stocks to avoid. While the current oil crash has devastated downstream producers, midstream producers had managed to stay fairly stable until recently, and many of the majors have actually seen their downstream sectors growing.

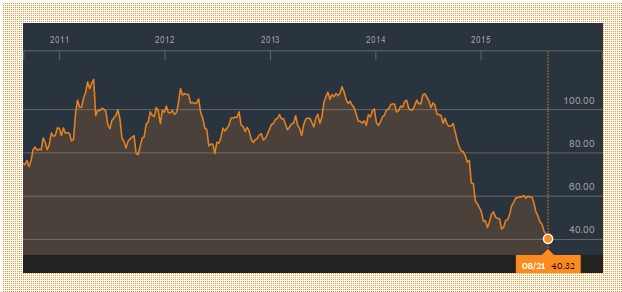

The above image should giving you a hint of what the oil crash has been like. After bouncing from $80 to $100 per barrel for the better part of half a decade, in mid-2014, oil began crashing and crashing hard. After forming a double bottom in January and March just under $50, it recovered to $60 for some time.

Then recently, fresh fears about slowing growth in China, along with the increasing chance of Iran moving huge amounts of oil to the market mean that prices have started tanking again. On August 21, oil prices briefly touched below $40 per barrel - the first time in a long time that they have gotten this low.

Despite all this, Phillips 66 (NYSE:

PSX) has remained strong. As a downstream oil company, it has not been as affected by the crash, which is reflected in its stock price. In fact, the company has seen its stock price barely drop from $81 before the crash to its August 21 price of $76 per share - a drop of less than 10%.

Phillips 66 Financial Highlights

Now that we have talked some about the macro oil situation, along with how Phillips 66 specifically has done, it is time to delve into the company's financials.

The company has seen its EBITDA hover somewhere between growing and constant. It is worth pointing out that looking at refining quarter by quarter is a poor idea, since it tends to be cyclical on a year-over-year basis.

Still, taking the average of the company's 2013, 2014, and Q1 and Q2 2015 earnings, you'll see that the most recent quarter had above-average earnings. In fact, since 3Q 2014, right around the start of the oil crash, the company has not reported income noticeably below the average - only at the average or above.

This points to the company's continued ability to grow, despite a toughening overall oil situation.

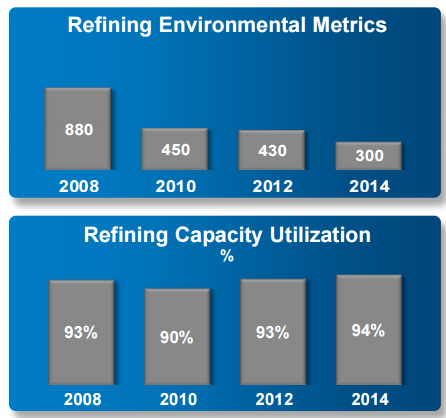

(Phillips 66 Utilization and Environmental Metrics - Phillips 66 Investor Presentation)

Part of this is due to the company's efficiency. Phillips 66 has managed to keep its refining capacity utilized at the low-to-mid 90% level, with the exception of a small drop-off in 2010. More so, on top of keeping its refining capacity constant, the company's environmental metrics (the effect it is having on the environment) have been decreasing.

Oil, compared to other forms of energy like solar and wind, is inherently dirty. The

recent protests about Shell (

RDS.A,

RDS.B) drilling in the Arctic should be enough to make investors understand the negative reactions people can have to energy sources that negatively affect the environment.

By decreasing its environmental impact, not only is Phillips 66 decreasing its chances of accidents and potential fines, it is also making itself more favored in the view of people and environmental groups. This should help support its business in the long run.

Strategy

Now that we have talked about the company's financial overview, it is time to talk about its strategy.

(click to enlarge)

(Phillips 66 Segment By Segment Strategy - Phillips 66 Investor Presentation)

The company operates in four different segments: midstream, chemicals, refining, and marketing and services. It is worth pointing out that out of these four segments, refining is by far the largest, followed by chemicals.

However, despite fluctuations in the other sectors, the company has always gained solid income from its marketing and specialties sector, and this sector will help provide the company with steady earnings.

In the midstream sector, the company is focusing on growing rapidly. It is using Phillips 66 Partners LP (NYSE:

PSXP) as a funding vehicle to help it raise capital, since the midstream tends to be a very capital-intensive business.

Most importantly, though, the company has announced its intentions to pursue organic and M&A (merger & acquisition) opportunities.

With many midstream pipeline companies seeing their stock prices take significant hits from 30% to more than 50%, now would be the time for the company to take a significant stance in the midstream space by purchasing a major company in the area.

In the chemicals sector, Phillips 66 is planning on advancing its projects, while growing organically. The company is also planning on taking advantage of several advantages it has, namely domestic feedstock and proprietary technology.

These things should allow it to continue growing in this sector.

In the refining sector, the company's most significant, Phillips 66 is looking to increase its yields and export capacity, while enhancing its portfolio. To me, enhancing your portfolio sounds like fancy talk for looking to acquire additional properties, should the opportunity present itself.

Purchasing additional refineries, especially if the company can grow its selling to customers (marketing and specialities) along with its transport (midstream) capabilities, will provide Phillips 66 with enough vertical integration to grow significantly.

Lastly, in the marketing and specialities category, the company is looking to grow its sale of lubricants. The company is also looking to expand into Europe. Europe has a number of large wealthy economies and should provide significant profits if the company is able to get a firm foothold.

Future Plans

Now that we have talked about the overall market along with the company's financial highlights and its current strategy, it's now time to talk about its future plans.

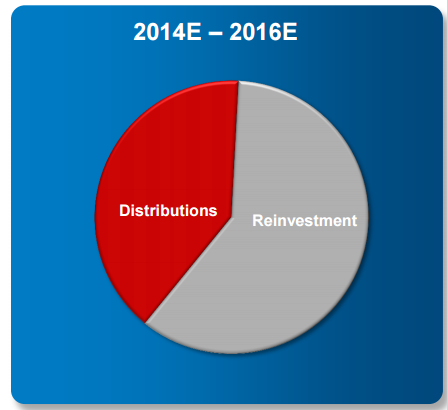

(Phillips 66 2014 through 2016 Distribution and Reinvestment Plans - Phillips 66 Investor Presentation)

The company's 2014-2016 plan involves the majority of its funds going to reinvestment in its business, with a significant portion of its funds paying its distributions.

The above graph makes me happy to see it. The reason for that is because if something should happen where the company sees its earnings draw, it is still a far way from having to cut its distributions.

During such a time of oil turmoil, I want to own companies that will pay me for the risk that I am taking. By covering its distributions by such a significant margin, should things go south, Phillips 66 will continue paying me for my risk.

(click to enlarge)

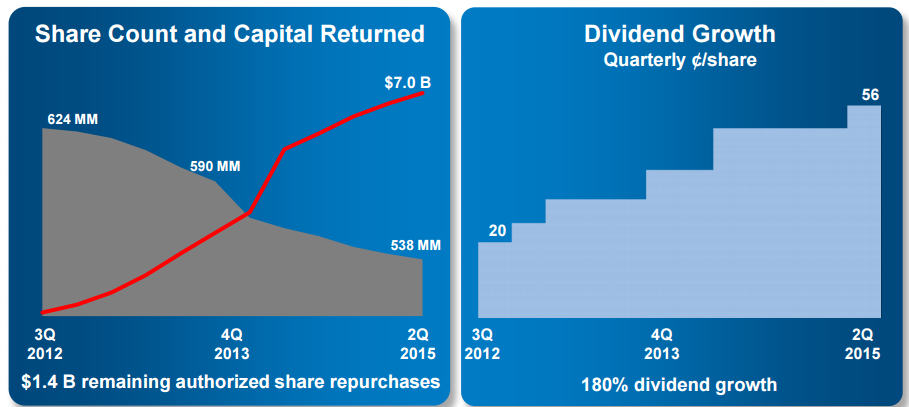

(Phillips 66 Dividend Growth and Buybacks - Phillips 66 Investor Presentation)

This strategy can be reflected in the company's history of helping shareholders. Since being split off from ConocoPhillips (NYSE:

COP), Phillips 66 has managed to almost triple its dividends, resulting in $7 billion of capital returned to shareholders.

More so, during this time, Phillips 66 has been buying back shares, managing to reduce its share count by an impressive 14%. It still has $1.4 billion remaining of authorized share repurchases, which should be enough for the company to decrease its share count by another 20 million or so.

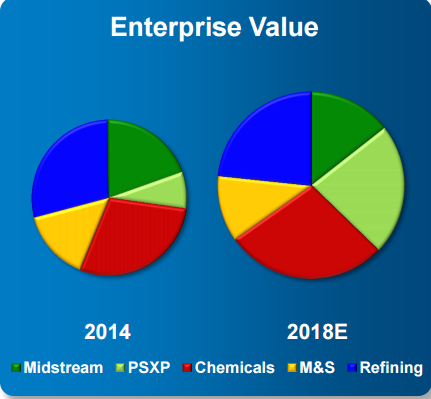

(Phillips 66 Enterprise Value Growth - Phillips 66 Investor Presentation)

More so, despite paying back so much to shareholders, it is still expecting to see its enterprise value grow. In fact, from 2014 to 2018, the company is expecting to see its EBITDA increase by more than 30%, driven mainly by the growing midstream sector.

All of these things together make Phillips 66 a solid buy in the current environment.

Conclusion

Phillips 66, despite its focus on the midstream and the downstream sectors, has seen its stock price fall in the past few days. However, despite this, it is a solid company with solid growth prospects.

The company is planning on heavily expanding in the midstream sector, potentially undertaking some expansions. It has a significant amount of potential ahead of it, and I expect it to continue growing in the long run.

More so, Phillips 66 has done an impressive job of rewarding shareholders. It has already managed to reduce its share count by 15%, and has the ability to increase it by several more percent with the current buyback plan. The company has also managed to triple its dividend since splitting off from ConocoPhillips three years ago.

These things together should help the company continue its growth and make it a solid investment in the oil market.