32,64 USD

+1,12% | +0,36

16/10/2015 16:14

@

Garmin: A Nice Option In The Wearables Space

Summary

While Fitbit has garnered most of the attention, Garmin makes for an intriguing option in the wearables space.

Garmin carries a forward P/E of 13, no long term debt and a dividend yield of over 5%.

Garmin is predictably seeing declining sales in auto GPS units but it seeing solid growth in both the fitness and marine sectors.

In a recent article I wrote, I offered up Garmin (NASDAQ:GRMN) as an alternative stock to own in the wearables space over the big current names like Fitbit (NYSE:FIT) and Apple (NASDAQ:AAPL). While Garmin's fitness wearable shipments are rising (up 40% year-over-year in Q2), it's the company's diversified product line that helps set it apart.

Garmin has long had a steady if not strong presence in the fitness area. While its product shipments are rising (their Forerunner line of watches are especially popular among runners) the company is still a distant 4th place in the market behind Fitbit, Apple and Xiaomi with just a 3.9% market share. But whereas Fitbit's primary focus is the fitness space, Garmin derives just 21% of its revenue from fitness.

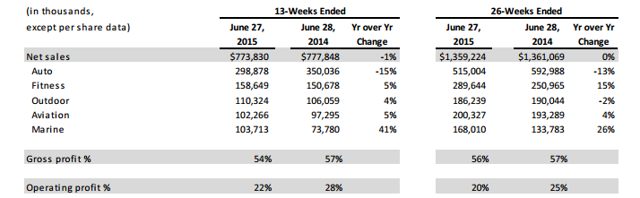

Garmin's big money maker not surprisingly is the automotive area where various versions of Garmin's Nuvi provide roughly 38% of the company's revenue.

(click to enlarge)

That number used to be 44% which would suggest on the surface that the company is becoming less of a one trick pony but the truth is that sales from auto are shrinking. Smartphones and other similar devices have become cheaper and easier to use alternatives to GPS hardware. Using the most recent data available, sales from auto are down 13% year over year which makes it that much more important that other areas pick up the slack.

Despite the fact that Garmin's overall share of the fitness wearables market is relatively small it's an area that is growing quickly and it's a reasonable assumption that growth will continue in this area. The other area that's seeing solid growth is the marine sector where its lineup of chart plotters, fish finders and radar modules has shown nice expansion in the past year.

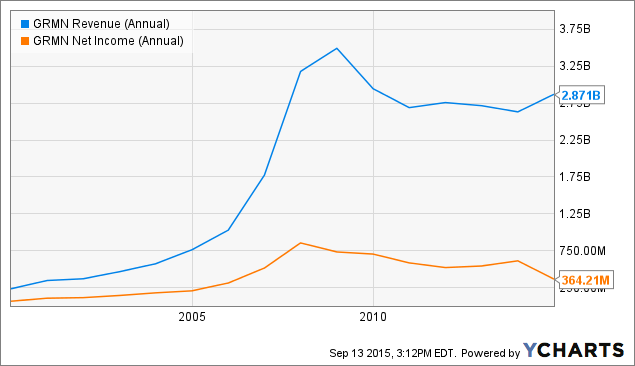

But one of Garmin's challenges is that overall revenues and earnings have flatlined over the past several years.

Since Garmin won't be confused for a growth stock any time it's more important to examine fundamentals to determine attractiveness. Garmin currently trades at a forward P/E of just 13 and a P/B of just a hair over 2 - both of which are very reasonable compared to the broad market - and carries no long term debt on its balance sheet. Income investors will be most intrigued by the stock's yield of over 5%. Part of the reason for that yield is the drop in the stock price over the last couple of years but management has committed to the dividend and has in fact been steadily raising it over the last several years.

Conclusion

While auto GPS sales will likely continue their steady decline it looks like Garmin will have other lines of business able to help make up for the shortfall. Its attractive valuation should help provide some downside protection and the dividend will look very attractive to income investors.

Fitbit has been the hot name in wearables and Apple has made its presence felt as well but as we've seen recently growth is not always rewarded. In scenarios like this a high dividend value name like Garmin might make the most sense.

Aucun commentaire:

Enregistrer un commentaire