ALCOA (AA)

13,08 USD

-0,98% | -0,13

10/04/2015 19:15

Alcoa (AA), le groupe d’aluminium, a dévoilé pour son premier trimestre 2015 un chiffre d’affaires de 5.8 milliards de dollars en hausse de 7% sur un an grâce principalement à ses activités dans l’automobile et l’aéronautique. Le résultat net est ressorti à 195 millions de dollars (0.14 dollar par action) contre une perte de 178 millions de dollars (0.16 dollar par action) au premier trimestre 2014. Le groupe table sur une hausse de 6.5% de la demande globale d’aluminium en 2015 à 57.5 millions de tonnes, un record. Pour 2014, Alcoa estime que la croissance de la demande a atteint 9% contre une précédente anticipation de 7%.

10,53 USD

-0,38% | -0,04

06/01/2014 22:01

3 Reasons Why Alcoa Is A Buy

Dec. 30, 2013 4:26 PM ET

The plunge in the prices of aluminum made 2013 a year to forget for miners like Alcoa (AA). Wide-scale aluminum users have long complained about the rising costs incurred as a result of delayed metal deliveries. As a result, the London Metal Exchange imposed a new set of rules through which the warehouses with the longest delivery time will see that time cut down to half, enabling them to deliver more aluminum than they can consume. This ultimately put more pressure on aluminum prices, which are already near a four-year low.

The reduction in prices has put downward pressure on Alcoa's share price; however, it has gained momentum since its latest earnings report. The key points of the report were:

· Net income jumped 116.8% year-over-year, rising from a loss of $143 million to a profit of $24 million.

· Cost of goods sold was 83.2% of total revenue, an improvement from 90.3% in the corresponding quarter of the previous year.

· Despite lower aluminum prices, the aluminum giant managed to post EPS of $0.11, which was above the industry average.

Getting a boost

Moreover, Goldman Sachs recently upgraded Alcoa's rating from neutral to buy. In addition, analyst Sal Tharani revised his price target upwards to $11. Tharani noted, "We estimate Alcoa will add more than $2bn of revenue and more than $525mn of additional EBITDA to its mid- and down-stream businesses over the next three years from end-market growth and share gains. Alcoa's downstream businesses, particularly Engineered Products, are less aluminum price sensitive and we see upside in Alcoa despite our lackluster outlook for aluminum supply-demand fundamentals. In addition, we see further upside beyond our current estimates from the automotive market through growth in "body-in-white" body sheet, as well as from aluminum-lithium in aero. Also, we expect continued productivity improvements and estimate positive free cash flow starting next year."

This report has further added to the stock's momentum. However, should you consider buying Alcoa at the current price? Let's take a look.

Solid productivity gains

The terrific quarterly performance was a direct outcome of the miner's productivity gain. According to Alcoa, it has already generated $825 million of savings on productivity improvements. This has helped the company to perform better than the industry average; however, does that mean that the aluminum giant's business is back on track? Maybe not. Alcoa's growth is noteworthy, but it does not solve the problem at hand -- low aluminum prices. Increasing productivity is only a short-term solution and you can't go on increasing it forever. The law of numbers will catch up and increasing productivity will become more and more difficult with the expansion of business.

Furthermore, aluminum prices are projected to remain well below the long-term price assumption of $2,250 a ton in each of 2013 and 2014, primarily because of the market's high inventory levels and production overcapacity.

What may drive growth?

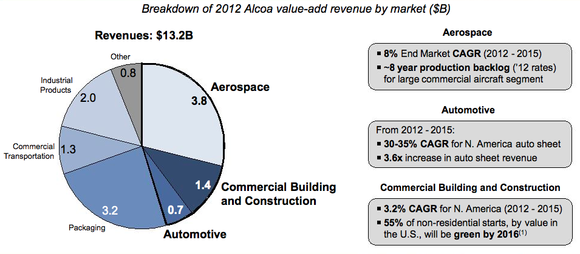

To fortify its position and drive long-term growth, Alcoa is switching its attention to niche specialty markets that should provide higher margins. Alcoa anticipates aerospace segment sales to grow 9%-10% in 2013, fueled by the enlarged backlogs of Boeing and Airbus. In fact, the miner has already signed a deal worth roughly $110 million to supply titanium and aluminum parts to Airbus.

(click to enlarge)

The company also expects the automotive industry to become more aluminum-centric, which would lead to a more than three-fold growth in revenue from this segment.

Growth across its niche markets, combined with cost controls, are the primary reasons why Alcoa's management is confident that it's on track to meet its yearly goal, which is to be cash-flow positive. Considering the fact that Alcoa's value-add business now accounts for nearly 57% of its revenue, it may be able to achieve its goal.

Conclusion

Alcoa is looking to add to its revenue going forward and is also focused on reducing costs. As the one of the largest producers of aluminum, Alcoa is well-positioned to benefit from the increasing usage of aluminum in different applications in aerospace and automotives. Thus, it won't come as a surprise if Alcoa maintains the momentum that it has gathered in the last three months into the New Year as well.

Aucun commentaire:

Enregistrer un commentaire